Software is no longer an emerging allocation in private credit. It is the allocation.

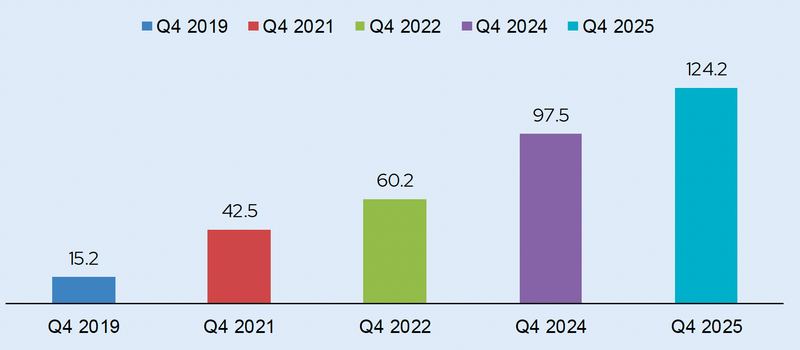

PRISM tracks $124.2 billion in software fair market value across 131 funds and 1,305 companies as of Q4 2025. Six years ago that number was $15.2 billion. The growth has been relentless, an 8x increase that shows no sign of slowing.

The scale is no longer the question. The question is whether the market's pricing framework has kept pace with the concentration risk it has built.

The Spread Is Too Narrow

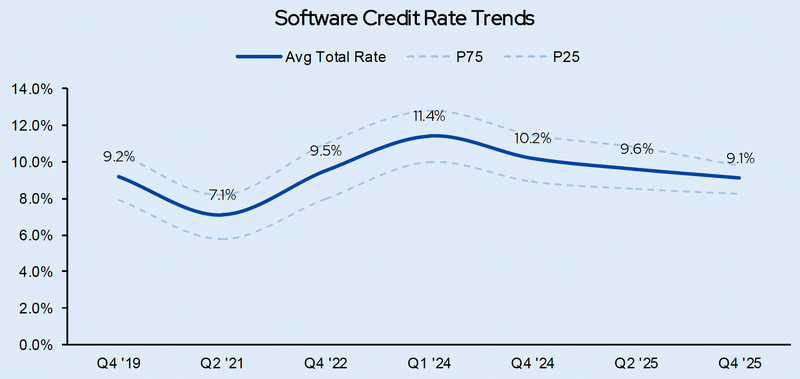

As software exposure has grown, rate dispersion has collapsed. The interquartile range across all software credits now sits at just 160 basis points. For a sector that spans core banking infrastructure to discretionary website builders, that band is remarkably tight. It implies the market is treating structurally different software credits as roughly interchangeable. They are not.

A borrower whose customers face three year migration cycles and regulatory lock in is not the same credit as a borrower whose customers can cancel with a click. But the spread between them says otherwise. The competitive pressure to deploy into familiar software names has tightened pricing on the most visible credits regardless of their underlying stickiness. Deal velocity has increasingly trumped credit differentiation.

The Maturity Wall Is Coming

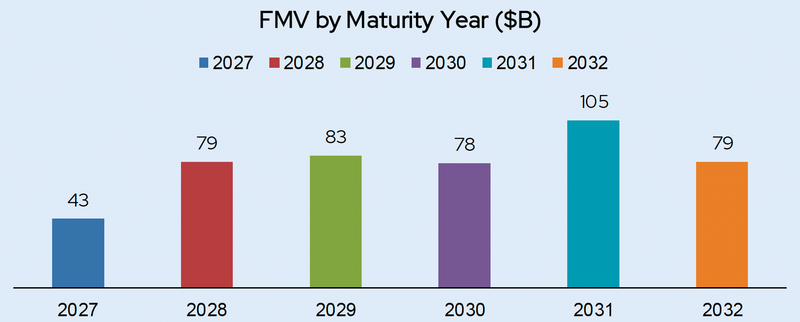

Software positions are heavily concentrated in the 2027 to 2032 maturity window. Over $467 billion in principal across nearly 37,500 positions will need to refinance during that period, with 2031 representing the single largest year.

These positions were originated in a market that did not distinguish between software archetypes. They will refinance into one that will have to. If credit conditions tighten or software fundamentals deteriorate unevenly, the refinancing experience for an infrastructure layer credit and a discretionary tool will look nothing alike. Lenders who have not classified their exposure by stickiness profile will discover the difference at exactly the wrong time.

We Have Seen This Before

The COVID quarter offers a small scale preview. In Q1 2020, the FMV to cost ratio across software positions dropped to 95.5%. But the aggregate masked a divergence that matters enormously for the current cycle: infrastructure layer software held value while discretionary tools did not. The lesson was cheap in 2020. Total software exposure was $15 billion and the market recovered quickly. Today the position is 8x larger and the maturity wall is approaching. The same divergence will play out again. The only question is whether lenders have built the framework to see it coming.

The market has built the position. It has not built the framework to manage it.

PRISM Private Credit Analytics provides institutional investors with proprietary data, analytics, and frameworks for private credit portfolio analysis. All data sourced from SEC filings aggregated through PRISM.