Private credit has two risk problems it is not solving. The first is crowding. The second is PIK. Both are visible in public data. Neither is being measured at the level that matters.

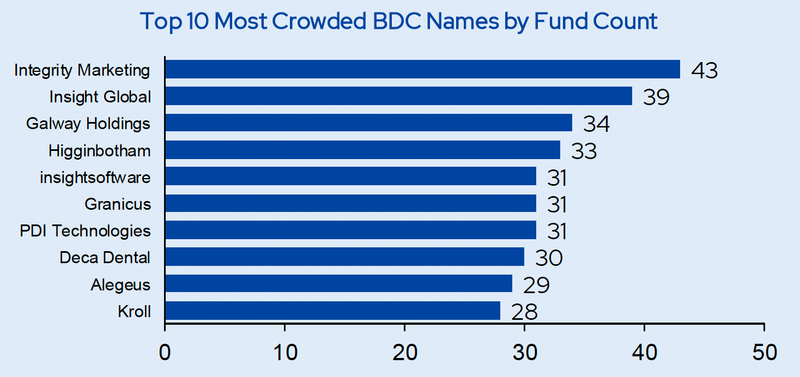

Start with crowding. The BDC universe grew from 61 funds to 143. Conventional logic says more funds means more diversification. The opposite happened. More funds chasing the same middle market borrowers produced more overlap, not less. The top 10 most crowded companies each sit in 28 to 43 separate BDC portfolios.

Three of the top ten are insurance brokerage roll ups. These are businesses built on the same thesis (recurring commissions are durable), financed by the same playbook (leveraged acquisition, private credit funded), and held across the same fund universe. Apollo, Ares, Blackstone, Blue Owl, Carlyle, Goldman, and KKR all hold positions in the same name. That is not diversification. It is a consensus trade with no exit coordination mechanism.

The industry treats this as an interesting data point. It is a structural vulnerability. In public markets, when a crowded trade unwinds, liquidity absorbs the shock across thousands of daily participants. In private credit, there is no secondary market, no real time pricing, and no shared visibility into who else holds the position. An unwind is a negotiation among 43 parties who did not know they were in the same room.

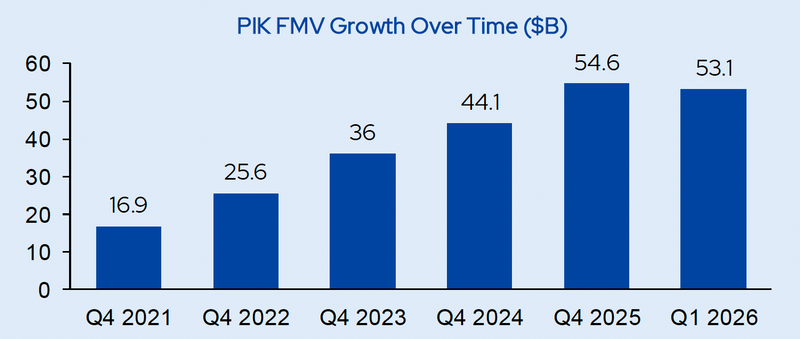

Now layer in PIK. Payment in Kind FMV tripled from $17B (Q4 2021) to $53B (Q1 2026). The market's explanation is that PIK has become a structural feature of deal design. Preferred instruments, structured transactions, negotiated payment flexibility. And for some positions that is true.

But the cross fund data says something harder to explain away. When one fund has a borrower on PIK, it might be structuring. When 27 of 31 fund holders have the same borrower on PIK, that is not structuring. That is a company that cannot generate enough cash to service its debt, and every lender in the syndicate knows it.

PIK positions carry an average FMV to par of 0.93, versus 0.97 for cash pay. The market is pricing in a 4 point valuation discount for PIK paper. That discount is the tell. If PIK were purely structural, the marks would be at par. They are not.

The defense of the current environment goes something like this: defaults are manageable, recoveries are reasonable, and the senior secured position protects against permanent capital loss. That may be true in isolation. But the crowding data and PIK data together say something the fund level view cannot: the risks are correlated in ways that no single manager's portfolio analytics can capture, because no single manager sees the aggregate.

If you are an LP allocating across multiple BDC managers, there is one question worth asking at every quarterly review this year: what percentage of your portfolio overlaps with your other BDC allocations, and how many of those shared positions are on PIK? If your managers cannot cross reference their books against the market, you are the only one who can demand it.

The full Private Credit Fact Book, with all charts and data tables, is available as a downloadable PDF.