The private credit market is enormous. It is also more concentrated than almost anyone realizes.

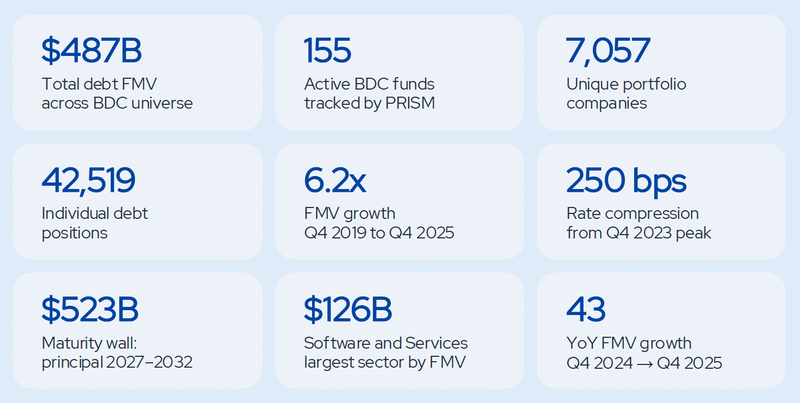

PRISM tracks $487 billion in fair market value across 155 BDC funds, 7,057 portfolio companies, and 42,519 individual debt positions as of Q1 2026. The conventional narrative is that this growth represents diversification. More funds, more borrowers, more sectors, more capital formation. The data tells a different story.

Three funds control 30% of the market. Blackstone Private Credit ($79B), Blue Owl Credit Income ($35B), and Ares Capital ($29B) collectively hold more FMV than the bottom 130 funds combined. The BDC universe did not diversify as it scaled. It consolidated.

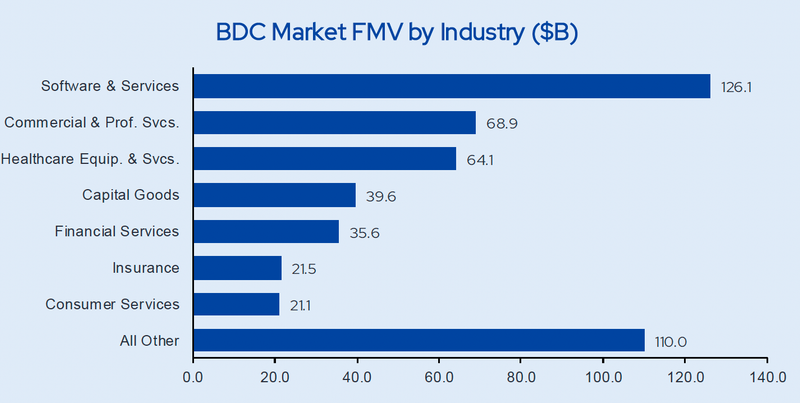

One sector controls 26%. Software and Services sits at $126B in FMV, more than double the next largest industry. Add Commercial Services ($69B) and Healthcare ($64B) and three industries capture 53% of the entire market. Every GP talks about sector diversification in their investor letters. The aggregate data says the industry is making the same bet.

Insurance tells the most revealing story of all. Just 138 companies generate $21.5B in exposure, the highest FMV per company ratio of any sector. This is not organic industry growth. It is the brokerage roll up trade, replicated across dozens of funds, financed almost entirely by private credit. The market built a massive concentrated position in a single business model and called it diversification.

The capital structure reinforces the pattern. First Lien anchors at 87.4% of total FMV ($425.6B). That sounds safe until you realize it means 155 funds are all lending senior secured into the same sectors, often to the same companies, at increasingly similar terms. Senior secured concentration is still concentration.

The question this raises is straightforward. A market that grew 6.2x in six years did not build 6.2x more infrastructure for understanding what it owns. Fund level reporting shows each manager their own portfolio. Nobody sees the aggregate. Nobody sees that 43 funds hold the same insurance brokerage, or that software is a quarter of every book, or that three funds have quietly become systemically important.

If you are an LP reviewing BDC allocations, the action item is simple: ask your managers what percentage of their portfolio companies appear in 20 or more other BDC funds. If they cannot answer the question, they do not have the data. That is the problem.

The full Private Credit Fact Book, with all charts and data tables, is available as a downloadable PDF.