There is a version of the private credit story where everything works out. Rates normalize gradually. Borrowers refinance smoothly. Fund returns compress modestly but remain attractive relative to public credit. Defaults stay manageable. That is the version the market is currently pricing.

The PRISM data suggests the margin for error has never been thinner.

Average BDC portfolio rates peaked at 11.6% in Q4 2023. Six quarters later they sit at 9.1%. That is 250 basis points of compression while the Fed delivered far less in actual cuts. The market moved first, with new originations at tighter and tighter spreads diluting legacy book yields faster than base rates declined.

Normally, tighter spreads slow origination. Lenders get disciplined. They wait for better entry points. That did not happen. Q4 2024 posted 4,326 new positions, the highest single quarter on record. Q2 2025 followed at 4,051. Capital deployment actually accelerated into the compression. This is the late cycle combination that credit investors are supposed to fear: more capital, thinner margins, same borrower universe.

Every cycle produces this setup. The question is never whether discipline erodes. It is how long the erosion runs before something forces a repricing.

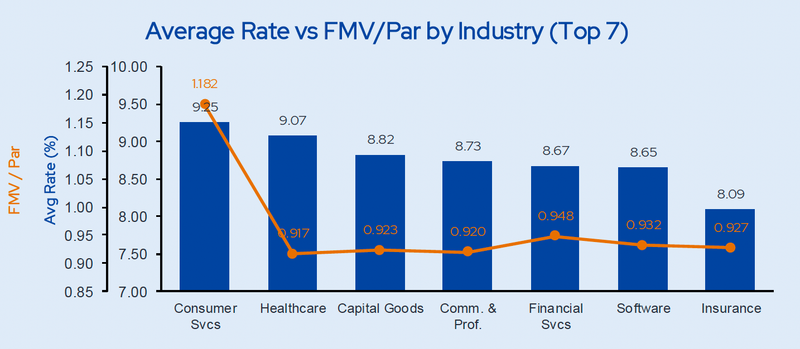

The sector level data shows the stress fractures are already visible if you know where to look. Healthcare credits carry a 9.07% average rate, which looks like adequate compensation until you see the FMV to par ratio: 0.917. That is the lowest of any top sector. Lenders are collecting a solid coupon while simultaneously marking the paper below par. When the rate says “moderate risk” but the mark says “I don’t fully trust the principal,” one of those signals is wrong.

Consumer Services sits at the opposite extreme: widest spreads (9.25%) but the richest FMV to par (1.18). The market apparently believes consumer facing businesses are riskier but worth more. That is an unusual combination and worth interrogating.

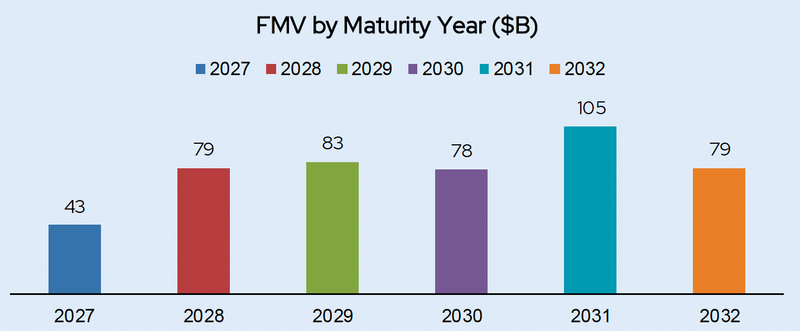

Now layer in what is coming. $523B in principal matures between 2025 and 2032. The peak hits in 2031 ($115B) and 2032 ($106B), but real pressure starts building in 2028 ($82B). Companies that borrowed at 11%+ in 2022 and 2023 will attempt to refinance into a 8 to 9% market. For strong credits that is a welcome reprice. For credits that used PIK to avoid cash pay shortfalls or rolled covenants to delay reckoning, it is the moment the music stops.

FMV on 2025 maturities already sits at 67 cents on the dollar. That is not a warning. That is the outcome for borrowers who could not get it done.

If you are a GP preparing for the 2028 to 2031 refinancing window, stress test your book at 200 basis points of additional spread compression and a 15% decline in EBITDA simultaneously. If the coverage ratios break, the maturity wall is your problem, not a market statistic.

The full Private Credit Fact Book, with all charts and data tables, is available as a downloadable PDF.